Every meaningful thing I've accomplished in my life began with a teacher who believed in me.

Professor Gary Gaile saw something in a restless college student studying geography and Japanese—two subjects that seemed to have nothing in common. He encouraged me to spend my youth traveling the world. My wanderlust turned into four years as a Goodwill Ambassador overseas, teaching English, coordinating international events, and learning that the best solutions come from truly understanding people first, systems second.

When I eventually found my way to financial planning, I knew exactly who I wanted to serve.

The people who spend their lives opening doors for others. The educators who believe in potential even when it's hard to see. The teachers who shape futures but often sacrifice their own.

If you're an educator, I'm not here to sell you products. I'm here to help you build a retirement plan that honors the work you've done.

WHY I SPECIALIZE IN EDUCATOR RETIREMENT PLANNING

Most financial advisors talk about serving educators. I actually did it—at scale—for years.

When I joined VALIC in 2010, I was assigned some of the most challenging territories in Texas: school districts with low participation, "dead" groups that previous advisors had given up on, and universities where educators were drowning in confusing options.

I thrived in that complexity.

In four years with VALIC, I:

- Became the 2011 Central Region Advisor of the Year

- Opened several new K-12 groups, including two 457 plans and a ROTH 403(b)*

- Reopened dozens of school districts that were considered "lost causes"

- Became a National Basic and Advanced Sales Trainer (they called us "Field Experts")

- Served on the National Field Advisory Board

- Won multiple national contests for enrollment and production

But here's what matters more than the awards: I learned to speak your language.

I understand why a teacher with 27 years in the classroom still isn't sure if she can afford to retire. I know why the pension calculation feels like solving a calculus problem with half the formula missing. I've sat with hundreds of educators who juggled summer income gaps, managed multiple retirement accounts they didn't choose, and worried about healthcare coverage before Medicare kicks in.

In 2014 I became an independent advisor with the intention of helping educators achieve financial freedom. When I started Texas Retirement Planners in 2017, I brought all of that experience with me—and I've never stopped focusing on the educators who gave me so much. As a result, my firm is able to work with public school and higher education employees throughout Texas.

THE PLANNING CHALLENGES ONLY EDUCATORS FACE

Your financial life is different from private sector employees, and you need an advisor who understands exactly how different:

**The TRS Pension Puzzle**

Your Teacher Retirement System pension is your foundation, but the calculation involves years of service, salary averages, retirement factors, your Tier and coordination with Social Security. Missing small details in these calculations can have a meaningful impact on your lifetime retirement income.

**The 403(b) vs. 457 Decision**

Most educators have access to both, but which one should you fund? How do the distribution rules differ? What happens if you leave education? When is the 457 more appropriate than the 403(b)? These aren't simple questions, and the wrong choice costs you real money.

**Summer Income Gaps**

You might be paid for 10 months of work but need 12 months of income. How do you build emergency reserves, maximize retirement contributions, and still manage cash flow when your paychecks stop every summer?

**Healthcare Before Medicare**

You're 58 and ready to retire, but Medicare doesn't start until 65. Seven years of healthcare coverage could cost $100,000 or more. How do you bridge that gap without derailing your retirement?

**Multiple Beneficiaries & Pension Decisions**

Should you take the maximum pension or the survivor benefit? What happens to your spouse if you pass away first? How do you coordinate your pension decision with life insurance, TRS-Care, and your other assets in a community property state? And God forbid, what if you were divorce. How does that affect the final outcome?

I've answered these questions hundreds of times—and every answer is unique to the person asking.

HOW I WORK WITH EDUCATORS

I don't do cookie-cutter financial plans. I've never believed in them.

Before I became an advisor, I spent over a decade as a management consultant, walking into struggling businesses and diagnosing what was broken. I learned to ask questions others didn't think to ask, see patterns others missed, and find solutions in complexity.

When I work with educators, I bring that same forensic approach:

**Step 1: Understand Your Story**

We start with your story, not your account balance. Where are you now? Where do you want to be? What concerns keep you up at night? What does a successful retirement actually look like for you?

**Step 2: Analyze Your Complete Picture**

I gather everything—TRS statements, 403(b) accounts, 457 plans, Social Security estimates, insurance policies, beneficiary designations, pension options. Then I analyze it all together, looking for gaps, inefficiencies, and opportunities others have missed.

**Step 3: Create Your Custom Strategy**

I build a comprehensive plan that coordinates every piece: optimal retirement date, income strategy, tax minimization, healthcare coverage, estate planning, and beneficiary coordination. Everything works together.*

**Step 4: Implement & Monitor**

We execute the plan, consolidate accounts where it makes sense, align your investments, and establish a system for ongoing monitoring and adjustment. Your financial life gets simpler, not more complicated.

**Step 5: Stay Connected**

I remember your milestones, check in during market volatility, and reach out proactively when tax laws change or planning opportunities arise. We're in this together for the long term.*

MY COMMITMENT TO EDUCATORS

I work with a lot of educators. It's not a sideline or a marketing niche—it's a core part of my practice and my purpose. I'm committed to providing the following comprehensive services:

**Retirement Income Planning**: Coordinate TRS, Social Security, and personal savings into a sustainable income strategy

**403(b) & 457 Optimization**: Maximize tax-deferred retirement accounts with educator-specific strategies*

**Investment Management**: Purpose-based portfolios aligned with your timeline and goals

**Tax Strategy**: Minimize lifetime taxes through strategic Roth conversions, distribution planning, and benefit coordination*

**TRS & Social Security Coordination**: Navigate pension calculations, WEP reductions, and survivor benefits

**Estate & Beneficiary Planning**: Protect your family and coordinate pension decisions with life insurance and legacy goals

**Cash Flow Management**: Strategies to smooth income throughout the year and build emergency reserves

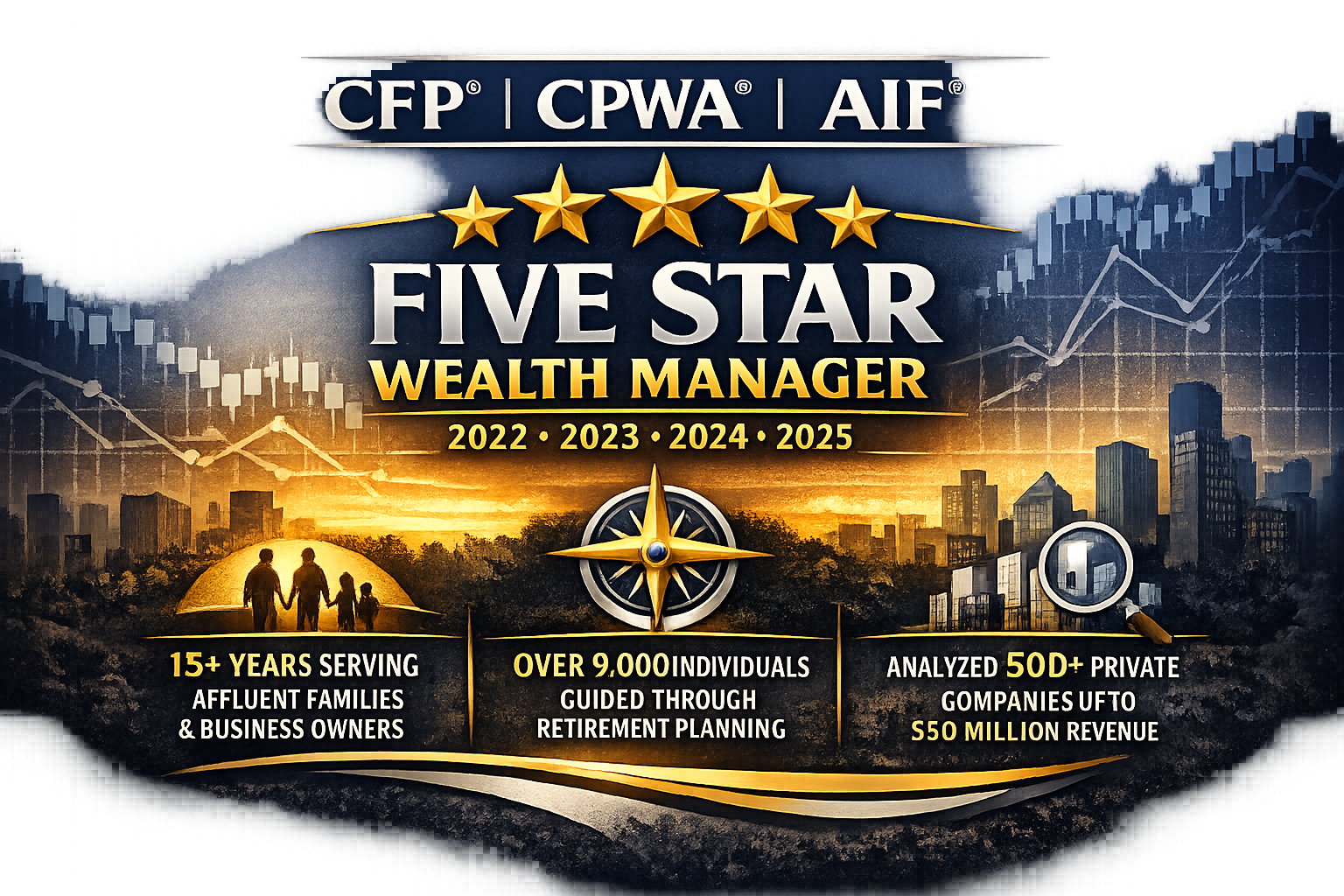

MY CREDENTIALS

- CFP®

- CPWA®

- AIF®

- Five Star Wealth Manager (2022, 2023, 2024, 2025)*

- 15+ years serving educators across Texas.

- Over 9,000 individuals guided through retirement planning.

YOUR NEXT STEP

If you're an educator wondering if you can afford to retire—or when, or how—let's talk.

I offer a complimentary initial consultation where we'll:

• Review your current situation

• Discuss your retirement goals and concerns

• Identify planning opportunities specific to your circumstances

• Determine if working together makes sense for both of us

No sales pressure. No obligation. Just a conversation about your future.

Schedule time with me today using the link below:

Book 403b Appointment Consultation

*Disclosures:

A distribution from a Roth IRA is tax-free and penalty-free provided that the five-year aging requirement has been satisfied and one of the following conditions is met: age 59 1/2, death, disability.

Information provided should not be considered as tax advice from GWN Securities, Inc. or it's representatives. Please consult with your tax professional.

The "Five Star Wealth Manager" award is administered by Crescendo Business Services, LLC's dba Five Star Professional ("Five Star"). Richard Becker is not affiliated with Five Star. Five Star does not endorse Texas Retirement Planners, GWN Securities, Inc. or any of its representatives. Candidates must satisfy ten (10) objective Eligibility Criteria and Evaluation Criteria associated with work. Factors taken into account include assets under management and client retention rate. Candidates also undergo a thorough regulatory and complaint review. Consumer survey feedback is insignificant in the overall award selection process. After receiving the respective award, representatives have the option of paying a separate fee to Five Star in exchange for publication of this information. The fee is not a condition precedent to receiving the award.